What Happens If the Buyer Stops Paying?

If you're worried about default, it helps to think like a bank, not a landlord. The two paths — evicting a tenant vs. reclaiming the property as the note holder — are very different in stress, cost, and outcome.

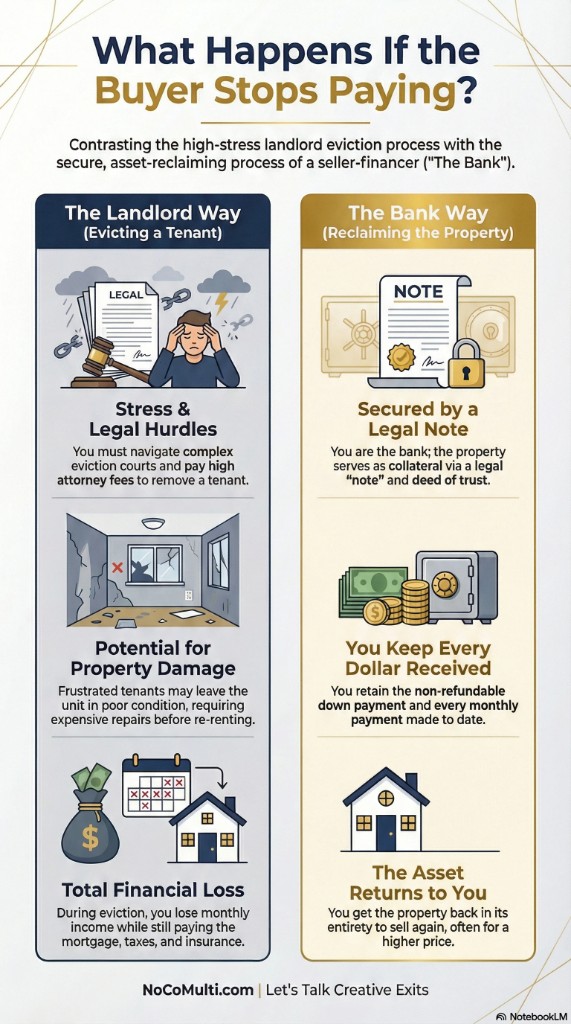

The Landlord Way: Evicting a Tenant

As a landlord, you must navigate complex eviction courts and pay high attorney fees to remove a tenant. Frustrated tenants may leave the unit in poor condition, requiring expensive repairs before re-renting. During eviction, you lose monthly income while still paying the mortgage, taxes, and insurance — a total financial squeeze.

The Bank Way: Reclaiming the Property

When you seller-finance, you are the bank. The property serves as collateral via a legal note and deed of trust. You retain the non-refundable down payment and every monthly payment made to date. If the buyer defaults, you get the property back in its entirety to sell again — often for a higher price. You're secured by the asset, not dependent on a slow eviction process.

Ready to explore your exit? Let's talk creative terms.