The Rate Squeeze Timeline: Why Traditional Sales Are Stalling

A guide to navigating high interest rates with creative seller financing. When bank rates exceed what properties can support, the conventional buyer pool shrinks — and seller financing becomes the fix.

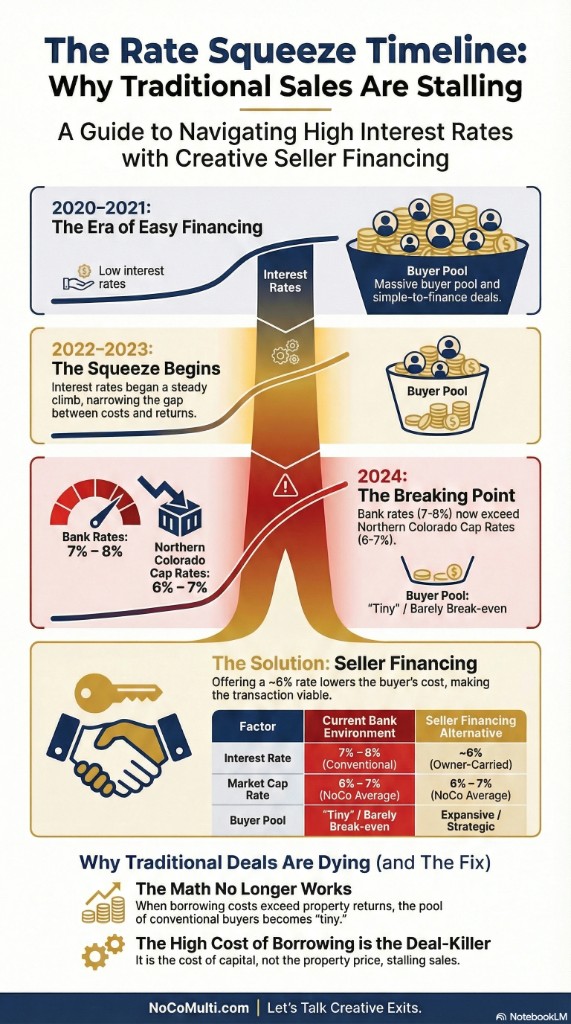

From Easy Money to the Squeeze

In 2020–2021, low interest rates meant a massive buyer pool and simple-to-finance deals. By 2022–2023, rates began a steady climb, narrowing the gap between borrowing costs and property returns. In 2024, bank rates (7–8%) now exceed Northern Colorado cap rates (6–7%). The result: a "tiny" buyer pool and deals that barely break even for conventional buyers.

The Solution: Seller Financing

Offering a rate around 6% lowers the buyer's cost and makes the transaction viable. You're not cutting the price — you're offering flexible terms. The math no longer works when borrowing costs exceed property returns; the high cost of capital is the deal-killer. Seller financing restores a broader, more strategic buyer pool.

Ready to explore your exit? Let's talk creative terms.