Subject-To (SubTo) and Assumable Mortgages

If you have an existing mortgage — especially a low interest rate from earlier years — the buyer can assume your payments instead of getting a new bank loan. That can make the deal work for both of you: you get out, they get a rate the bank can't offer.

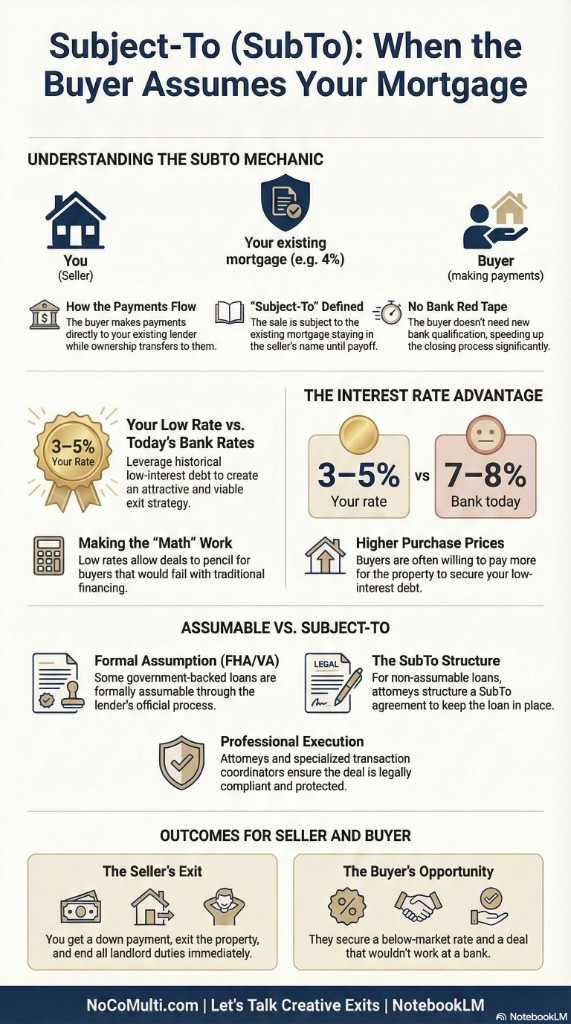

What is Subject-To (SubTo)?

In a subject-to sale, the property is sold "subject to" your existing mortgage: the buyer takes over the payments (and often takes possession or receives the deed under an agreed structure) while the loan stays in place in your name until it's paid off or the buyer refinances. It's a common creative-financing structure when you don't own free and clear but still want to exit without waiting for a traditional bank buyer.

Why It Can Be "Even Better"

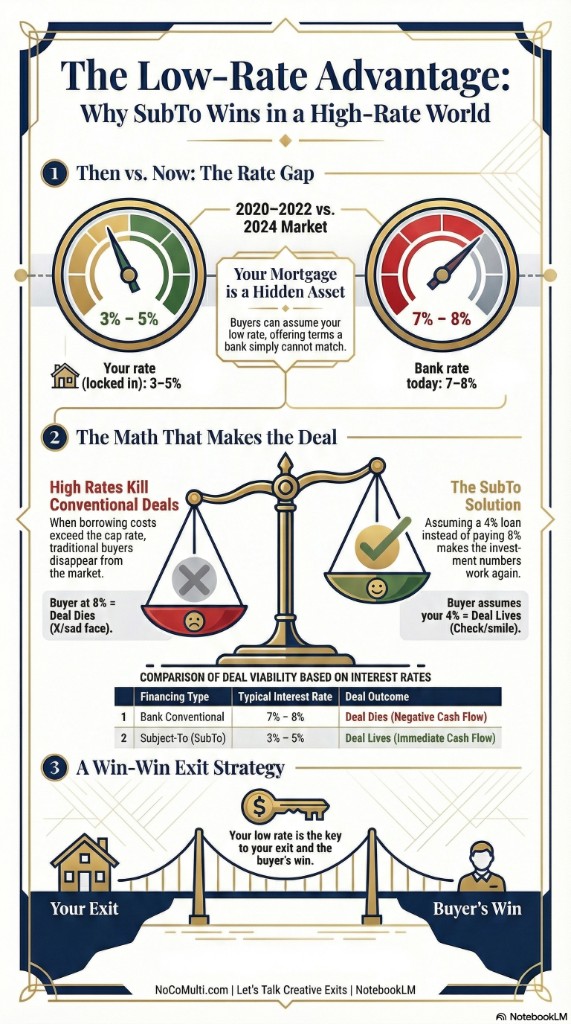

When your mortgage rate is lower than today's bank rates — for example, you locked in 3–5% in 2020–2022 and banks are now at 7–8% — the buyer assumes that lower rate. Their payment is smaller, so the numbers work for them. You get a down payment, exit the property, and move on without landlord duties. In that sense, SubTo can be an even stronger outcome than pure seller financing: your low rate becomes the deal-maker.

Assumable vs. Subject-To

Some loans are formally assumable (e.g. many FHA and VA loans), meaning the lender allows a qualified buyer to take over the loan. Others are done as subject-to: the buyer agrees to make the payments; you and your attorney structure the sale and any second note or agreement. Either way, your existing low rate can make the sale possible when a bank loan wouldn't.

Due-on-Sale and Professional Advice

Many mortgages have a "due-on-sale" clause that allows the lender to call the loan if the property is sold. Investors and attorneys often structure subject-to deals with clear agreements and risk allocation. We don't give legal advice — we recommend talking to a real estate attorney who understands creative financing in Colorado so your exit is structured correctly and safely.

Already own free and clear? You can still do seller financing (you carry the note). If you have a mortgage and want to explore SubTo, we can point you in the right direction.

See our FAQ on seller financing and mortgages →Ready to explore your exit? Let's talk creative terms.